Audits are a fundamental part of governance, risk, and compliance frameworks. However, one of the most frequently searched and often misunderstood terms in auditing is “auditee.” Understanding who the auditee is, their responsibilities, and their role in the audit process is essential for ensuring audit effectiveness and compliance readiness.

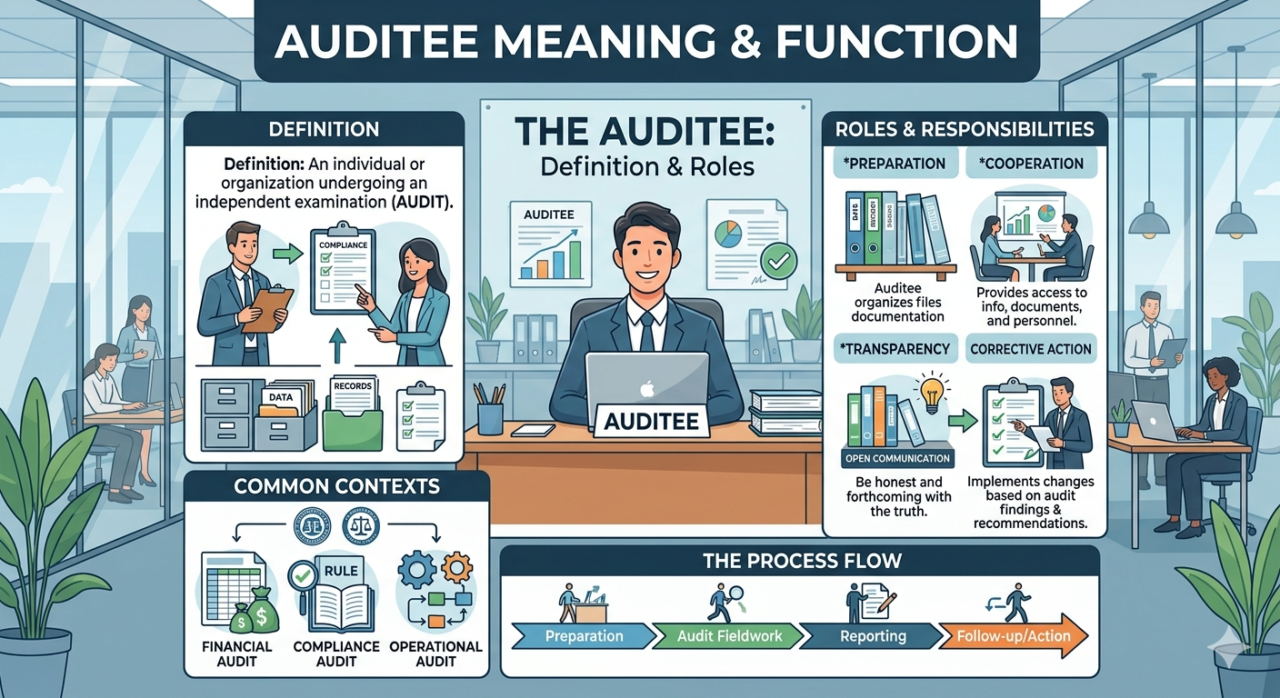

Auditee refers to the individual, department, or organization that is being audited. The auditee is responsible for providing information, evidence, and responses required by auditors to evaluate compliance and controls. Without effective auditee participation, audits cannot deliver reliable outcomes.

This guide provides a complete framework for understanding the auditee’s role—from definition and responsibilities to audit lifecycle participation, common challenges, best practices, and how GRC automation transforms the auditee experience from reactive document collection to proactive audit readiness.

1. What is Auditee in Audit? Definition and Core Meaning

An auditee is the entity being evaluated during an audit. The auditee can be:

- An individual (e.g., a process owner or department manager)

- A department or business unit (e.g., IT, Finance, HR, Operations)

- An organization (e.g., a subsidiary, vendor, or third-party partner)

- A process or system (e.g., payroll processing, customer onboarding)

The auditee:

- Provides documents and supporting evidence required for the audit

- Responds to auditor queries and requests for clarification

- Demonstrates adherence to policies, procedures, and regulations

- Supports audit execution by facilitating access, interviews, and walkthroughs

- Implements corrective actions to address identified findings

In simple terms, the auditee is the subject of the audit process—the person or group whose activities, controls, or compliance posture is being examined.

2. Role of an Auditee in the Audit Process

The auditee plays a central, active role in the success of any audit. Far from being a passive subject, the auditee’s engagement directly impacts audit quality, efficiency, and outcomes.

Key roles of the auditee include:

- Facilitating audit activities: Scheduling interviews, providing workspace access, coordinating with team members

- Providing accurate and complete information: Sharing documentation, data extracts, and evidence in a timely manner

- Supporting auditors during evaluation: Answering questions, demonstrating processes, explaining controls

- Clarifying processes and controls: Helping auditors understand how systems and procedures actually operate

- Implementing corrective actions: Addressing audit findings and closing identified gaps

The effectiveness and efficiency of an audit largely depend on the auditee’s preparedness and cooperation. A proactive, well-organized auditee can reduce audit duration by 30-50% and significantly improve outcomes.

3. Key Responsibilities of an Auditee

An auditee is responsible for ensuring that audit requirements are met efficiently, accurately, and completely. These responsibilities span the entire audit lifecycle.

1. Provide Accurate and Complete Information

All documents, data extracts, and responses provided to auditors must be accurate, complete, and up to date. Incomplete or inaccurate information leads to audit delays, additional findings, and potential qualification.

2. Maintain Proper Documentation

Policies, procedures, control records, evidence logs, and approval trails should be well-maintained, version-controlled, and readily accessible. Poor documentation is a common source of audit findings.

3. Ensure Compliance with Policies and Regulations

The auditee must demonstrate adherence to internal policies, industry standards, and regulatory requirements. Compliance is not optional—it must be evidenced.

4. Respond to Audit Queries in a Timely Manner

Provide clear, complete, and timely responses to auditor requests. Delayed responses extend audit duration and can indicate control weaknesses.

5. Implement Corrective Actions

Address audit findings by developing and executing remediation plans. Track closure of identified gaps and provide evidence of completed actions to auditors.

6. Designate a Primary Audit Contact

Assign a knowledgeable point of contact who can coordinate audit activities, gather evidence, and serve as the liaison between auditors and the auditee team.

4. Auditee vs Auditor: Understanding the Key Differences

While both auditee and auditor are essential to the audit process, their roles, responsibilities, and objectives are fundamentally different.

| Aspect | Auditee | Auditor |

|---|---|---|

| Primary Role | Being audited – subject of evaluation | Conducting the audit – performing evaluation |

| Core Responsibility | Provide evidence, information, and access | Evaluate controls, identify risks, test compliance |

| Objective | Demonstrate compliance and control effectiveness | Provide independent assurance and identify gaps |

| Reporting Relationship | Reports to management / business leadership | Reports to audit committee / board / regulators |

| Independence | Not independent – part of the area being audited | Independent – objective and impartial |

| Key Action After Findings | Implement corrective actions | Verify remediation and update findings |

Key takeaway: The auditor evaluates the organization, while the auditee enables that evaluation by providing the required inputs, access, and evidence. Both must work collaboratively for an effective audit.

5. Auditee Involvement Throughout the Audit Lifecycle

The auditee is involved throughout the entire audit lifecycle—not just during fieldwork. This continuous involvement ensures audit accuracy, completeness, and efficiency.

Phase 1: Planning Stage

The auditee provides initial information, scope inputs, process documentation, and access requirements. Participates in opening meetings and risk assessments.

Key activities: Share process flows, identify key contacts, confirm scope, schedule interviews

Phase 2: Fieldwork Stage

The auditee shares requested evidence, supports testing activities, participates in walkthroughs, responds to auditor questions, and provides clarifications.

Key activities: Submit documentation, demonstrate controls, attend interviews, answer queries

Phase 3: Evaluation Stage

The auditee clarifies observations, provides additional evidence as needed, and explains any anomalies or exceptions identified by auditors.

Key activities: Respond to preliminary findings, provide supplemental evidence, explain process variations

Phase 4: Reporting Stage

The auditee reviews draft audit findings for factual accuracy, provides management responses, and commits to corrective action timelines.

Key activities: Validate findings, draft management responses, assign action owners, set due dates

Phase 5: Closure / Remediation Stage

The auditee implements corrective actions, provides evidence of remediation, and participates in follow-up or validation audits as required.

Key activities: Execute action plans, submit remediation evidence, track closure status

This structured involvement ensures that audits are efficient, accurate, and collaborative rather than adversarial or fragmented.

6. Examples of Auditee: Real-World Scenarios

Understanding who the auditee is in different audit contexts helps clarify the concept.

Bank IT Audit

A bank’s IT department is being audited for cybersecurity compliance, access controls, and change management. The IT department (and its managers) is the auditee.

Internal Audit – Finance Department

Internal audit reviews the finance department’s financial controls, reconciliation processes, and segregation of duties. The finance team and its leadership are the auditee.

Third-Party / Vendor Audit

A bank audits a cloud service provider for SOC 2 compliance and security controls. The vendor organization is the auditee.

Regulatory Audit – Anti-Money Laundering (AML)

A central bank examines a financial institution’s AML compliance program. The entire bank is the auditee, with the AML compliance officer as primary contact.

Process Audit – Loan Origination

Internal audit reviews the loan origination process for compliance with underwriting policies. The lending operations team is the auditee.

7. Why the Auditee is Critical to Audit Success

The auditee is not a passive participant—they are essential to audit effectiveness. Without effective auditee participation, audits cannot deliver reliable outcomes.

- Provides the evidence required for evaluation: Auditors cannot test controls or verify compliance without auditee-provided documentation and access

- Enables verification of compliance: The auditee demonstrates how policies and controls operate in practice

- Supports transparency and accountability: Open collaboration builds trust and enables honest gap identification

- Helps identify and address control gaps: Auditees often have the deepest understanding of process weaknesses

- Contributes to process improvement: Audit findings, when embraced by auditees, drive operational improvements

- Reduces audit duration and cost: Prepared, responsive auditees complete audits 30-50% faster

- Improves audit ratings: Cooperative auditees with well-documented controls receive better assessments

In short: Auditors evaluate, but auditees enable. Neither can succeed without the other.

8. Common Challenges Faced by Auditees

Auditees often encounter significant challenges that make audit participation stressful and inefficient.

- Lack of centralized documentation: Evidence scattered across shared drives, emails, paper files – difficult to locate and share

- Delays in responding to audit requests: Manual gathering of evidence takes days or weeks – extends audit duration

- Limited understanding of audit requirements: Unclear what evidence is needed or how to present it effectively

- Difficulty tracking audit findings: Spreadsheets and email threads lose status updates and evidence of closure

- Manual and fragmented processes: No single system for request management, evidence submission, or response tracking

- Last-minute fire drills: Auditors request additional evidence with tight deadlines – disrupts normal operations

- Inconsistent audit history: Unable to see what was requested or provided in prior audits – repeated requests

- Audit fatigue: Multiple audits (internal, external, regulatory, customer) with overlapping requests – no coordination

These challenges result in audit delays, increased findings, higher costs, and unnecessary stress for auditee teams. They also create audit risk when evidence cannot be produced in a timely manner.

9. Best Practices for Auditees: Preparing for Audit Success

Implement these best practices to transform the auditee experience from reactive and stressful to proactive and confident.

1. Centralize Documentation

Maintain all audit-related information—policies, procedures, evidence, control records—in a single, accessible, and searchable repository. Eliminate scattered files and email attachments.

2. Understand the Audit Scope

Clearly define what is being audited, which processes and systems are in scope, and what evidence will be required. Review the audit program and request clarification before fieldwork begins.

3. Assign Clear Ownership

Designate a primary audit coordinator who serves as the single point of contact. Assign evidence owners for each request. Ensure accountability throughout the audit lifecycle.

4. Prepare in Advance

Keep documentation ready before audit initiation. Conduct pre-audit self-assessments. Identify potential gaps proactively and address them before auditors arrive.

5. Track Audit Findings Systematically

Use a structured system to track audit findings, management responses, action owners, due dates, and remediation evidence. Monitor closure status continuously.

6. Respond Promptly and Completely

Address auditor requests as soon as possible. Provide complete, accurate evidence the first time. If delays are unavoidable, communicate proactively and set expectations.

7. Build a Collaborative Relationship

Treat auditors as partners, not adversaries. Open communication and transparency lead to better outcomes. Ask questions when requirements are unclear.

8. Learn from Each Audit

After each audit, conduct a lessons-learned session. Identify what went well and what could be improved. Update documentation and processes accordingly.

10. Auditee Maturity Model: From Reactive to Audit-Ready

Assess your organization’s auditee capability using this five-level maturity model.

| Level | Name | Characteristics | Audit Experience |

|---|---|---|---|

| Level 1 | Reactive | No preparation. Evidence gathered during audit. Missed deadlines. Incomplete responses. High stress.), | Painful – delays, findings, extended duration |

| Level 2 | Aware | Basic documentation exists. Designated contact. Responds to requests but inconsistently. Spreadsheet tracking. | Stressful – evidence gaps, some findings |

| Level 3 | Structured | Centralized repository. Defined processes for request handling. Pre-audit self-assessments. Consistent responses. | Manageable – minor findings, predictable duration |

| Level 4 | Proactive | Automated request tracking. Real-time status dashboards. Continuous audit readiness. Evidence always available. | Efficient – minimal findings, smooth process |

| Level 5 | Audit-Ready Always | Integrated GRC platform. Real-time evidence access. Automated findings tracking. Continuous monitoring. Proactive gap closure. | Effortless – no surprises, audit-ready any time |

Most organizations operate at Level 2 or 3. Advancing to Level 4 and 5 requires automation and GRC integration.

11. How GRC Tools Transform the Auditee Experience

Manual audit processes using spreadsheets, email, and shared drives are difficult to manage at scale and create unnecessary stress for auditees. Modern GRC platforms transform the auditee experience.

Governance-Integrated Audit Management: GRC platforms link audit management directly to risk registers, control libraries, policy management, and compliance frameworks. When an audit finding identifies a control gap, the system automatically links to the relevant risk and can trigger policy updates or control remediation workflows—creating a closed-loop governance system.

Key GRC Capabilities for Auditees

- Centralized audit documentation: Single repository for all audit evidence, policies, and control records – always accessible

- Audit request management: Track auditor requests, assign owners, monitor status, submit evidence – all in one place

- Automated evidence collection: Link evidence to requests automatically. Reuse evidence across multiple audits

- Real-time status dashboards: See open requests, upcoming due dates, and overall audit progress at a glance

- Finding and action tracking: Centralized repository for audit findings, management responses, action plans, and remediation evidence

- Audit-ready reporting: Generate evidence packages, response summaries, and closure reports with one click

- Historical audit records: Complete history of past audits, requests, and evidence – no rework for recurring requests

- Collaboration tools: Comment threads, notifications, and approval workflows keep auditee teams aligned

Platforms such as Aspia help organizations improve audit readiness, reduce manual effort, and enhance compliance visibility – enabling a transition from reactive audit handling to structured, proactive compliance management.

12. Regulatory Context: Why Audit Readiness Matters

For banks and regulated enterprises, audit readiness is not optional – it is a regulatory requirement. The auditee’s preparedness directly impacts regulatory outcomes.

- Basel Committee on Banking Supervision: Requires banks to have effective internal audit functions and auditee cooperation

- RBI Guidelines (India): Mandates that auditees provide complete access and information to auditors – non-compliance is a regulatory violation

- OCC Heightened Standards (US): Requires large banks to demonstrate audit readiness and responsive auditee participation

- SOX Section 404: Requires management to provide evidence of controls to external auditors – auditee documentation is essential

- PCI-DSS Requirement 12: Requires organizations to maintain audit trails and evidence of compliance – auditees must produce on demand

- ISO 27001 Clause 9.2: Requires internal audit program with auditee cooperation and evidence provision

13. Frequently Asked Questions (FAQs)

What is an auditee in audit?

What is the role of an auditee?

What is the difference between auditee and auditor?

Can a department be an auditee?

Why is the auditee important?

How can auditees prepare for an audit?

What is audit readiness?

14. Conclusion: From Audit Subject to Strategic Partner

The auditee is a critical component of the audit process. Their role extends beyond merely providing information – they enable transparency, support compliance, and drive organizational improvement through effective remediation.

For banks and enterprises, a well-prepared auditee contributes to efficient audits, reduced risk, and stronger governance. When auditees embrace their responsibilities – maintaining documentation, responding promptly, and closing findings – audits become collaborative opportunities for improvement rather than adversarial compliance exercises.

Leveraging GRC platforms allows organizations to streamline audit processes, improve visibility, and maintain compliance at scale – transforming the auditee from a reactive, stressed participant into a proactive, audit-ready partner in governance.

Transform Your Auditee Experience with ASPIA

ASPIA provides a unified GRC platform that transforms audit management from reactive fire drills to proactive, continuous audit readiness. Our solution enables auditees to:

- ✓ Centralize all audit evidence in a single, searchable repository

- ✓ Track audit requests and responses with real-time status dashboards

- ✓ Manage findings, action plans, and remediation evidence

- ✓ Link audits directly to risks, controls, policies, and compliance frameworks

- ✓ Generate audit-ready evidence packages with one click

- ✓ Maintain continuous audit readiness – not just at audit time

- ✓ Reduce audit preparation time by up to 70%

Move from reactive audit stress to proactive, confident audit readiness.

Request an ASPIA Demo